Understanding Financial Hedging for renewable energy projects: A Guide for lawyers and non-lawyers

And why do we call it hedging?

In the world of enegy projects and energy markets we all hear the term “hedging”, but what does this actually mean and why does it matter? If you’ve ever wondered about financial hedging in the context of Power Purchase Agreements (PPAs), this post breaks it down in simple terms.

The classic example on the developer side is that for bank financing (to make the project viable) you need to “hedge” the output of the wind / solar farm under a long term contract. On the buyer side, utlity and corporate, each needs to hedge for different reasons. The utility or trader has a number of open “positions” (put a pin in that) and is constantly fixing prices with counterparties. The corporate has energy needs for which it pays a volatile price (especially since 2019 where we had dramatic lows (lockdowns) and dramatic highs (Ukraine - Russia war). For many corporates with significant energy demand, a fixed price for energy becomes easier for its wider corproate decisions (i.e. production, expansion).

This post sets out:

the basics; what is financial hedging in the world of renewable energy?

the financial risks hedging protects against

common hedging strategies in PPAs

a hedging cheat sheet summary

1. Breaking Down the Basics: What Is Financial Hedging?

Simple Definition:

Hedging is like insurance—it protects against financial losses caused by unexpected changes in market prices. And that’s why it derives from the word of physically planting a hedge, which protects our land from dangers (wild animals, burglars, nosy neighbours).Why It Matters in PPAs:

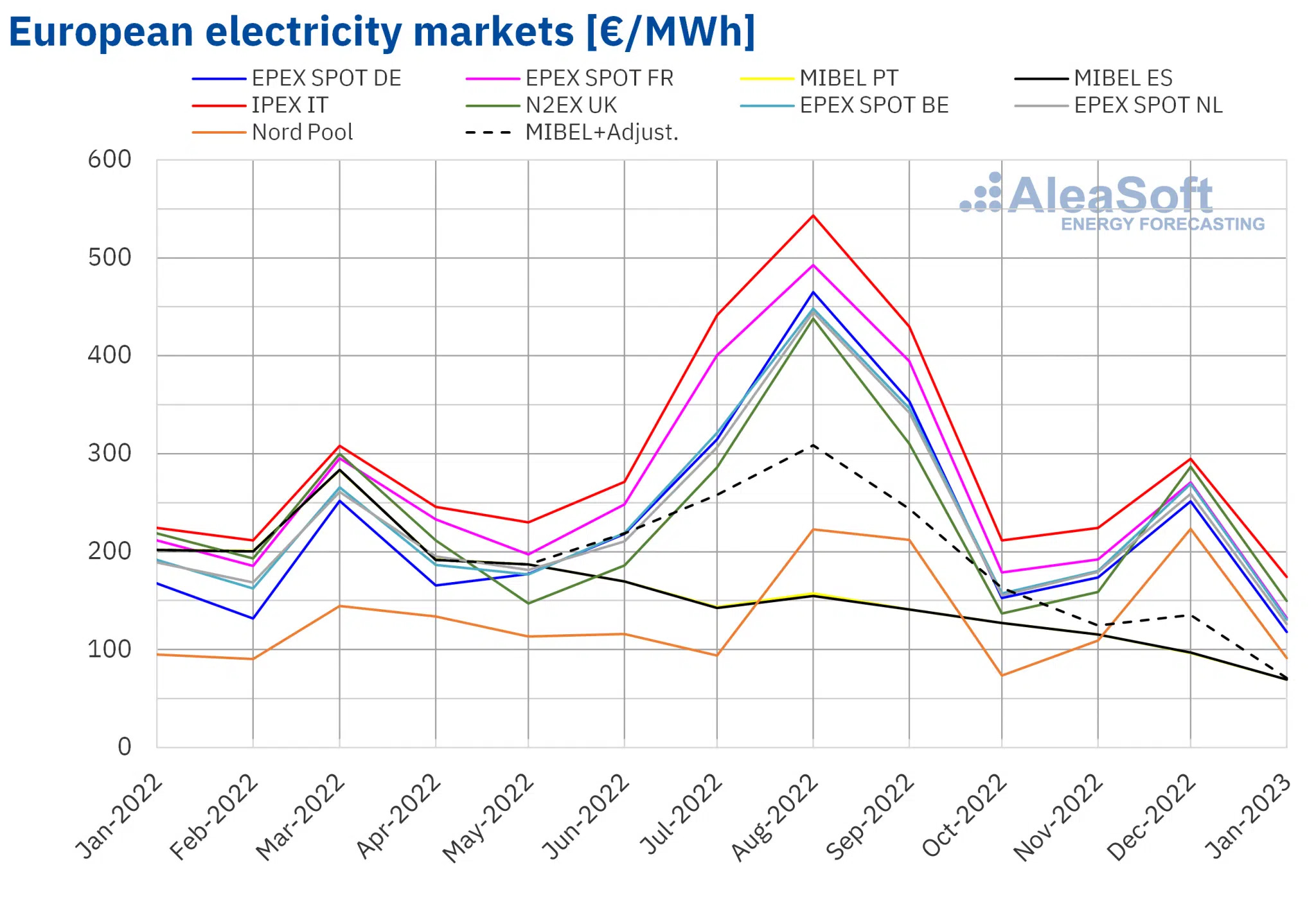

If energy prices were not volatile hedging would have little value. But as power prices are dependent on a host of factors, including, demographics, economic growth, natural resources (e.g. natural gas), physical infrastructure (e.g. lack of power transmisison or new gas pipelines), the weather, regulations (new incentive schemes, permitting restrictions, carbon pricing); the power price is anything but stable.Prices can swing from 50 (£, $, €)/MWh to 200/MWh. Both producers and offtakers therefore have an incentive to seek to hedge, or fix the price over long periods of time, at least for a certain percentage of their portfolio or demand. This helps manage the financial risks of this volatility for both buyers and sellers.

Key Players in Hedging:

🏢 1. Corporate Buyers (Offtakers)

These are typically large corporations purchasing renewable energy through PPAs to meet sustainability goals or lock in long-term energy prices.

Roles in Hedging:Risk Management: Hedge against energy price volatility to ensure cost predictability.

Contract Structuring: Work with advisors and financial institutions to structure hedging agreements (e.g., Contracts for Differences or VPPAs).

Sustainability Targets: Ensure that hedging aligns with environmental and corporate social responsibility goals.

🌿 2. Developers (Energy Project Owners)

These are the companies or entities responsible for a combination of all or some of building, owning, and operating renewable energy projects like wind farms or solar plants.

Roles in Hedging:Revenue Security: Use hedging strategies to guarantee stable revenue streams regardless of market price fluctuations.

Contract Negotiations: Work with buyers to agree on PPA terms that balance risks and rewards for both sides.

Financing Support: A well-hedged PPA can help secure project financing at attractive rates by ensuring a predictable cash flow.

⚡ 3. Utility Buyers

These are traditional energy companies that purchase power to resell it to end-users (residential, commercial, or industrial customers).

Roles in Hedging:Price Stability: Hedge energy purchases to offer stable pricing to their customers and protect against market volatility.

Portfolio Management: Balance various energy sources (renewables, fossil fuels, etc.) to manage supply and demand effectively.

Long-term Procurement: Enter into PPAs with developers to secure long-term renewable energy at fixed or predictable rates, helping meet regulatory requirements for clean energy.

Risk Mitigation: Use hedging to reduce the risk of supply disruptions or regulatory penalties related to renewable energy targets.

🔄 4. Energy Traders

These are specialized market participants (who may also have utility dvisions, such as EDF Trading, EnBW and Axpo) who buy and sell energy commodities for profit, often operating independently or as part of large financial institutions or utilities.

Roles in Hedging:

Market Liquidity: Facilitate energy transactions by matching buyers and sellers in both physical and financial markets.

Speculative Hedging: Use advanced hedging strategies to profit from market movements while providing liquidity to others.

Arbitrage Opportunities: Exploit price differences across markets or time periods, which indirectly supports corporate buyers and developers in managing risks.

Custom Hedging Solutions: Offer tailored financial instruments (like swaps or futures) to help corporate buyers and developers hedge specific risks, such as basis risk or seasonal fluctuations.

🏦 5. Banks and Lenders

Financial institutions that provide the capital needed to finance renewable energy projects.

Roles in Hedging:

Loan Security: Require hedging mechanisms as a condition for lending, to ensure the project's financial viability (and ability to pay back the loan).

Risk Assessment: Analyze how hedging affects cash flow stability and loan repayment risk, with a bias towards long-term contracted revenue.

Collateral Management: Use hedged agreements as collateral for securing loans or reducing borrowing costs.

💰 6. Financial Institutions and Hedging Providers

These include investment banks, insurance companies, or specialized hedge funds that offer financial products for risk management.

Roles in Hedging:

Hedging Instruments: Provide products like swaps, options, or Contracts for Differences (CfDs) that mitigate financial risks.

Market Expertise: Offer analysis and insights on energy markets to help structure effective hedging deals.

Liquidity Providers: Ensure there’s enough liquidity for large corporate buyers or developers to enter into and exit from hedging agreements.

📑 7. Legal and Financial Advisors

Specialized law firms and consultancy firms focused on structuring PPAs and hedging arrangements.

Roles in Hedging:

Contract Drafting: Ensure contracts accurately reflect the hedging terms and risk allocation.

Regulatory Compliance: Help navigate complex legal frameworks around energy trading and financial hedging (e.g. EMIR).

Risk Assessment: Advise on the financial implications of various hedging strategies.

🔍 8. Energy Market Operators

Entities like grid operators or independent system operators (ISOs) that manage energy markets.

Roles in Hedging:

Market Pricing: Set real-time and forecasted market prices, which directly affect hedging strategies.

Settlement Support: Facilitate the financial settlement of hedging contracts based on actual market conditions.

3. The Financial Risks Hedging Protects Against

Below are the most common risks to be cosnidered under a financial hedge.

Price Risk: Market prices are volatile. By fixing a price under a fPPA both parties are hedging this risk. Practically speaking, if a wind farm fixes the price at which it’s paid at EURO 60/MWh, this means that if the power price then trends below this, it’s protected and if the power price trends above the 60 its “losing” out on upside. The key here is not to consider a loss or gain but to find a figure at which both buyer and seller feel comfortable with over the duration of the contract, despite the ups and downs of the market, which will undoubtabdly occur.

Volume Risk: Especially for renewables and even more so for wind this is a real risk. Wind speeds are highly volatile and we’ve seen in recent years that it’s becoming “less windy”, whether this is temporary or a structural change due to climate change. The ideal for the producer is that there are no volume guarantees. That said the buyer will often want a certain minimum volume, either for hedging purposes or to ensure it receives the green energy it’s after (corporates). The key here is to find a number both parties are happy with. This probably deserves a post on its own to distibguish between development and operational projects (where you have real historical data) and between solar and wind. Essentially the producer needs to set this minimum at an amount it’s very comfortable it can meet as otherwise financial penalties will apply.

Basis Risk: This relates to markets where pricing differs by region. This can be found in individual coutnries such as Italy and Sweden but also on a pan-EU and pan-US basis. Here the risk is that the price of electricity at the delivery point (buyer’s location) differs from the market price at the producer’s location. For example, there are a number of corporate buyers of solar PPAs in Spain who are based (or their consumption is based) in other Member States, such as Germany. Settlement is done at OMIE (Spanish wholesale market) which trades much lower than the German wholesale market. However in such a case the corproate may be buying the power for the Guarantees of Origin and is comortable with this “basis risk”. There is no one size fits all solution and much will depend on the specific market and the sophistication and bargaining power of each counterparty.

Credit Risk: It’s no surprise that one of the most heated discussions in PPA negotiations is the credit risk of each party. In short, as financial PPAs foresee payments being made both ways, each party must provide comfort to the other that it can live up to its financial obligations. This will be tested against different price scenarios. The advantage in such a relationship as opposed to a lender - borrower relationship is that in developed, liberalised markets, there are plenty of options for each of the buyer and seller in case the counterparty defaults and becomes insolvent.

Negative Pricing: this is fast rising up the list of risks facing both sides of a financial hedge. Zero and negative pricing is becoming very common in most of Europe as the share of solar and wind deployments goes up. The way it’s dealt with in a hedge will impact the pricing and will depend on the counterparties ability to deal with this risk. What we are frequently seeing is a floor price, below which the buyer will not pay the seller the fixed price, or an ability for the seller to stop generating (and therefore avoid paying the offtaker). I will return to negative pricing in a new post.

4. Common Forms of Hedging

Government Contract for Differences (CfD): In this scenario, which exists in a number of countries, including the UK, Italy and France, a goverment entitty agrees a “strike” price wtih a project developer, let’s say EUR70/MWh. Wheneevr the wholesale market rpice (which the project receives when it exports electricity) is below 70, it receives a top up from the counterparty. When prices are above 70, the developer pays the difference to the counterparty. Think of this mechanism not as a PPA but as a price stability mechanism. This mechanism has been a hugely innovative structure allowing a very fair compesnation to producers while ensuring that when prices are high consumers receive the reward. Another advantage is that it’s based on a standard form contract which avoids lengthy and expensive negotiation.

Fixed-Price PPAs: This is a straightforward way for producers to export physical power they receive and receive a fixed price by the utility offtaker . It combines both a physical and financial element in the contract. That said, these contracts are typically for a much shorter tenor than 10 years. .

Virtual PPAs (VPPAs): These don’t involve physical delivery but allow companies to hedge against price fluctuations as described above already. They can be bespoke vPPAs (of fPPAs) or based on standard form documentation such as an ISDA or EFET. Such contracts are considered derivatives and must comply with certain financial regulatory requirements.

7.Hedging Cheatsheet

8. Conclusion: Hedging as a Tool for Stability

Hedging is a fundamental tool in renewable energy markets, helping both buyers and sellers navigate price volatility. Whether through long-term PPAs, CfDs, or financial instruments, effective hedging strategies ensure financial stability and project viability. As energy markets evolve, new challenges like negative pricing will require even more sophisticated hedging approaches.

Stay tuned for a deep dive into negative pricing in an upcoming post!